Let’s Explore Savings Accounts that Earn the Lowest Returns in 2023

Introduction: Demystifying Savings Accounts and Making Smart Choices

Saving money is an essential aspect of financial well-being, but with so many options out there, it’s no surprise that people become quickly overwhelmed. In this blog post, we’ll dive into the world of savings accounts and reveal which savings account will earn you the least money. By understanding the pros and cons of the different types of accounts out there, you’ll be better equipped to make the best decision for your own financial goals. So, let’s dive right in!

Which Savings Account Will Earn You the Least Money?

A quick snapshot:

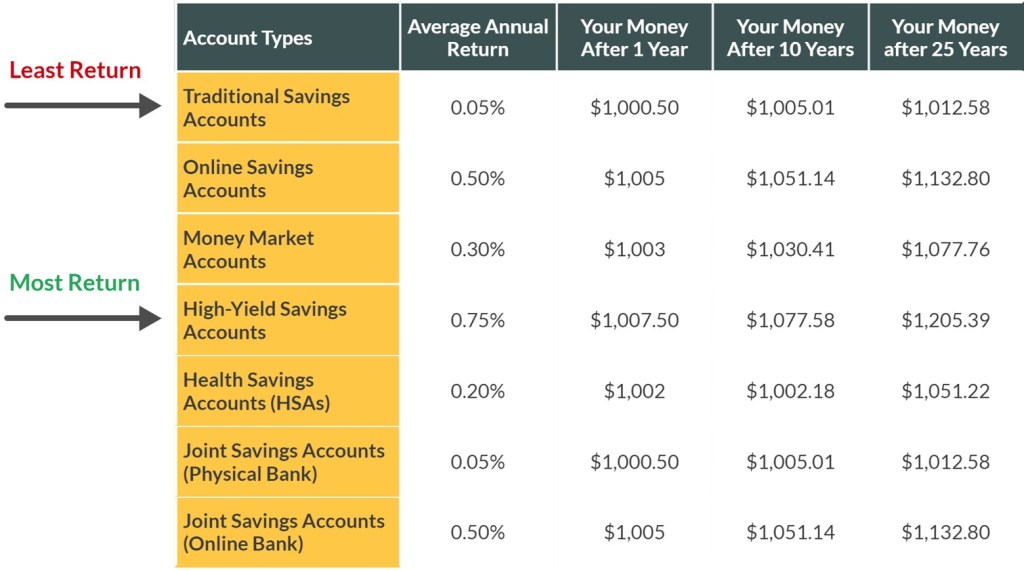

“If I invested $1,000 in each type of account, how much would I earn?”

Traditional Savings Accounts: Familiar Faces with Lower Returns

Average Annual Return: 0.01% to 0.1% –> (This savings account will earn you the least money)

A. The Basics of Traditional Savings Accounts

Most physical banks provide traditional savings accounts, which have been around for a very long time. Although they might be a well-known option, these accounts frequently have the lowest interest rates, so your savings won’t grow much over time. Traditional savings accounts do have some advantages, such as FDIC insurance and the ease of in-person banking services, despite their reduced earning potential.

B. Evaluating Traditional Savings Accounts

Weighing the benefits and drawbacks of a regular savings account is crucial. Even if they might not offer the best returns, these accounts can nevertheless be a suitable choice for investors who value accessibility and the security of a reputable bank. Compare interest rates, fees, and account features across several banks and account types to make the best option possible.

Online Savings Accounts: The Digital Age’s Answer to Saving

Average Annual Return: 0.4% to 0.6%

A. The Rise of Online Savings Accounts

Online savings accounts have grown in popularity as a result of the expansion of digital banking. Because online banking has lower overhead costs than traditional banking, these accounts typically offer higher interest rates than their traditional counterparts. To be sure, thoroughly consider your selections because not all online savings accounts are created equal.

B. Choosing the Right Online Savings Account

When evaluating online savings accounts, pay attention to interest rates, fees, and account minimums. Some accounts may have hidden costs that could really reduce your earnings. Additionally, consider the convenience and customer service options offered by each bank, as the lack of physical branches may be a drawback for some users. Some people like having the option to go into their bank to ask for assistance in person.

Money Market Accounts: A Middle Ground for Savers

Average Annual Return: 0.2% to 0.4%

A. Understanding Money Market Accounts

Money market accounts offer a middle ground between interest earnings and accessibility. These accounts generally have higher interest rates than traditional savings accounts and usually include features like the ability to write checks and to have debit cards. However, their interest rates still tend to be lower than those of high-yield online savings accounts.

B. Assessing Money Market Accounts

Before opening a money market account, you should check the account minimums, fees, and withdrawal limitations. Due to a regulation called “Regulation D”, these accounts may have limits on the number of monthly withdrawals and transfers. Ensure the money market account you choose aligns with your unique financial goals and estimated utilization of the account.

High-Yield Savings Accounts: The Quest for Maximum Earnings

Average Annual Return: 0.5% to 0.7%. –> (Highest Average Return)

*However, some online banks may offer rates above 1% during promotional periods or under certain conditions

A. The Appeal of High-Yield Savings Accounts

For those seeking the highest returns on their savings, high-yield savings accounts are a popular choice. These accounts, which are frequently provided by internet banks, are meant to offer the highest interest rates. High-yield savings accounts may not all offer the same rates, and some may still produce lesser returns than others. Always check the details!

B. Selecting the Best High-Yield Savings Account

Compare interest rates, costs, and account features of various high-yield savings accounts to find the best one. Remember that compared to traditional banks, these accounts could offer less customer service and accessibility. A high-yield savings account may be the best choice if you’re at ease with internet banking and value high interest rates.

Health Savings Accounts (HSAs): Specialized Accounts with Limited Use

Average Annual Return: 0.1% to 0.3%

A. Exploring Health Savings Accounts

Health Savings Accounts (HSAs) are designed specifically for individuals with high-deductible health plans. These accounts offer tax advantages and can be used for medical expenses, but they’re not an ideal choice for general savings purposes. HSAs often have lower interest rates than other savings account options and using them for non-medical expenses can result in taxes and penalties.

B. Determining if an HSA is Right for You

If your primary goal is to save money for medical expenses and you have a high-deductible health plan, an HSA could be a valuable tool. However, if you’re looking for a savings account to maximize your overall earnings, it’s best to explore other options.

Joint Savings Accounts: Sharing the Wealth and the Responsibility

Average Annual Return: 0.01% to 0.1% for traditional accounts or 0.4% to 0.6% for online savings accounts, depending on the bank.

A. An Overview of Joint Savings Accounts

A joint savings account is one that is shared by two or more people, frequently a couple or family. Although they may not be the best option for maximizing earnings, these accounts offer the convenience of shared access and management. With the same institution, joint accounts typically have the same interest rates as individual accounts, so lower rates will also mean lower returns for joint account holders.

B. Deciding on a Joint Savings Account

Before opening a joint account, consider your financial goals and explore other savings options that may offer higher returns. If the convenience of shared access outweighs the potential for lower earnings, a joint savings account could still be a good choice.

Solved: Which savings account will earn the least money?

Making the best choice for your financial objectives requires a thorough understanding of the various savings account types and their earning potential. We discovered that the Traditional Bank Savings Accounts are savings accounts with the lowest earnings. Even though some accounts might give you a lower income than others, you should carefully weigh the benefits and drawbacks of each option. You can make an informed decision and improve your savings strategy by comparing interest rates, costs, and account features.

References:

Federal Deposit Insurance Corporation (FDIC): Information on insured banks and interest rates.

Consumer Financial Protection Bureau (CFPB): General information about savings accounts and how to choose the right one.

https://www.consumerfinance.gov/consumer-tools/savings/

Bankrate: A reputable source for comparing interest rates on various savings accounts.

https://www.bankrate.com/banking/savings/rates/

NerdWallet: Offers comprehensive information on different types of savings accounts, including high-yield savings and money market accounts.

https://www.nerdwallet.com/banking/best-savings-accounts

Investopedia: A resource for understanding Health Savings Accounts (HSAs) and their benefits.

https://www.investopedia.com/terms/h/hsa.asp

Forbes: An article discussing the pros and cons of joint savings accounts.

https://www.forbes.com/advisor/banking/pros-and-cons-of-joint-savings-accounts/

Leave a comment